The 20% Rule: How to Finance a Car You Can Actually Afford is gaining attention across the United States as rising vehicle prices and high interest rates push more buyers into financial stress. In 2026, many Americans are discovering that expensive car loans can consume a large portion of their monthly income, making it harder to save, invest, or manage everyday expenses. The 20% Rule is emerging as a simple strategy to help buyers avoid taking on more vehicle debt than they can realistically afford.

Why Car Affordability Matters More Than Ever

New and used vehicle prices remain significantly higher than they were just a few years ago. Combined with elevated financing rates, many buyers are stretching their budgets to purchase vehicles they cannot comfortably afford. Financial experts warn that oversized car payments can create long-term money problems. As a result, affordability is becoming a bigger priority than luxury features or brand prestige.

Understanding the 20% Rule

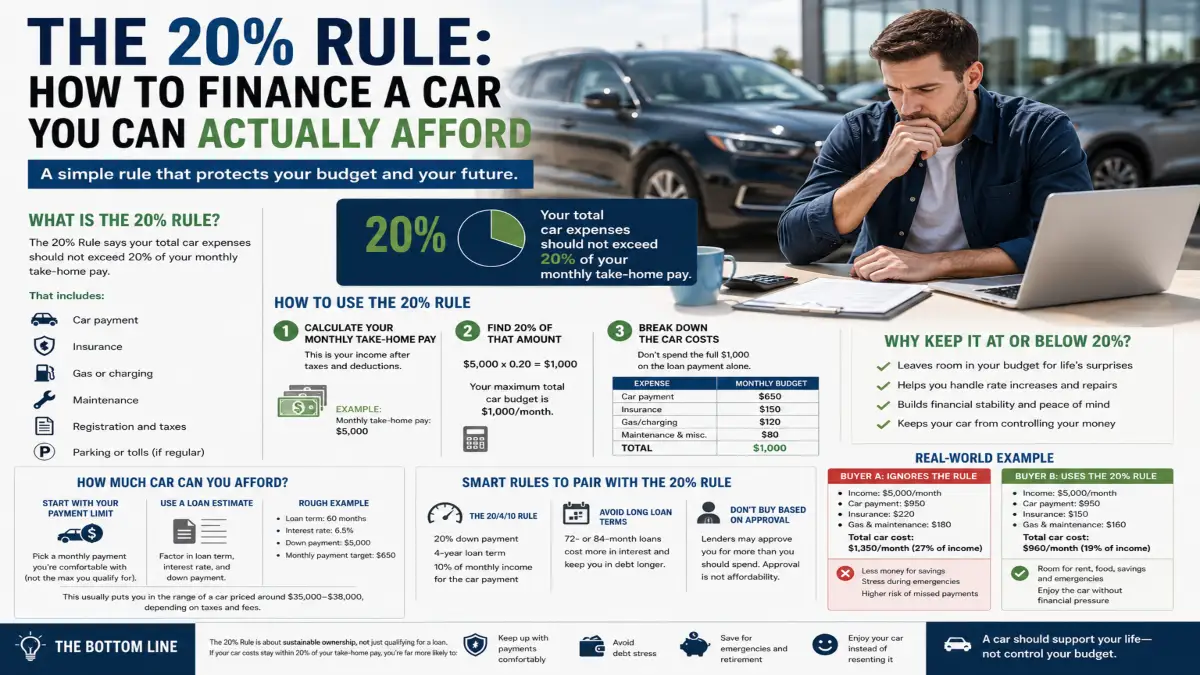

The 20% Rule is a budgeting guideline designed to prevent excessive vehicle spending. According to this approach, total transportation costs should remain within a manageable percentage of monthly income. Buyers are encouraged to focus on affordability rather than the maximum amount a lender is willing to approve.

- Make a substantial down payment when possible

- Avoid excessively long loan terms

- Keep monthly payments within budget limits

This strategy helps reduce financial pressure and long-term debt.

High Monthly Payments Can Hurt Financial Goals

Many Americans are committing to vehicle loans that exceed their comfort zone. Large monthly payments reduce the ability to build emergency savings, invest for retirement, or pay off existing debt. Financial flexibility often disappears when transportation costs consume too much income. This is one reason why affordability-focused car buying is becoming more popular.

Longer Loan Terms Create Hidden Risks

To make expensive vehicles seem affordable, lenders increasingly offer loans lasting six, seven, or even eight years. While this lowers monthly payments, it significantly increases total interest costs. Buyers may also end up owing more than the vehicle is worth for several years. Understanding the true cost of financing is critical before signing any agreement.

Smart Buyers Focus on Total Ownership Costs

Affordability extends beyond the monthly loan payment. Insurance, fuel, maintenance, registration fees, and repairs all contribute to the actual cost of vehicle ownership. Buyers who calculate these expenses before purchasing are less likely to experience financial strain. This broader approach helps create a more realistic vehicle budget.

Car Financing Scenarios in 2026

| Vehicle Type | Average Monthly Payment | Recommended Buyer Approach | Financial Impact |

|---|---|---|---|

| Compact Sedan | $450–$650 | Strong Affordability | Low Risk |

| Small SUV | $550–$750 | Budget Carefully | Moderate Risk |

| Mid-Size SUV | $700–$950 | Higher Income Needed | Moderate Risk |

| Full-Size Truck | $850–$1,200 | Large Budget Required | High Risk |

| Luxury Vehicle | $1,000–$1,800 | Significant Financial Commitment | Very High Risk |

Financial Freedom Starts with Smart Financing

The 20% Rule: How to Finance a Car You Can Actually Afford highlights the importance of making vehicle purchases that support long-term financial health. As car prices and borrowing costs remain elevated in 2026, more Americans are prioritizing affordability over status and unnecessary upgrades. A practical financing strategy can help buyers enjoy reliable transportation without sacrificing future financial goals.